Fleet Plan Implementation

- The vehicle replacement program should be reviewed annually as part of the budget process. Prior to budget preparation, the fleet manager (or other designated fleet administrator) and finance director should meet with each user department to review replacement priorities, evaluate fleet utilization, and update the multi-year replacement plan.

- When a vehicle or piece of equipment is placed into service, its estimated replacement cost, expected useful life, and annual replacement contribution should be established. User departments should make annual or periodic contributions to the Vehicle Replacement Fund based on these values. Contributions should be reviewed periodically and adjusted as replacement costs and expected service lives change.

- Proceeds from the sale or trade-in of surplus vehicles and equipment should be deposited into the Vehicle Replacement Fund to help offset inflation and reduce future replacement costs.

- The finance director should maintain accounting records for the Vehicle Replacement Fund and periodically provide department managers with reports showing replacement contributions, fund balances, and projected replacement schedules.

- When a vehicle reaches the end of its planned service life and has been approved for replacement through the capital budgeting process, funding should be provided from the Vehicle Replacement Fund.

- If a vehicle is destroyed or suffers a catastrophic loss, insurance proceeds should be applied toward its replacement. If replacement costs exceed available insurance proceeds and accumulated replacement funding, the remaining balance should be funded through other available sources as determined during the budget process.

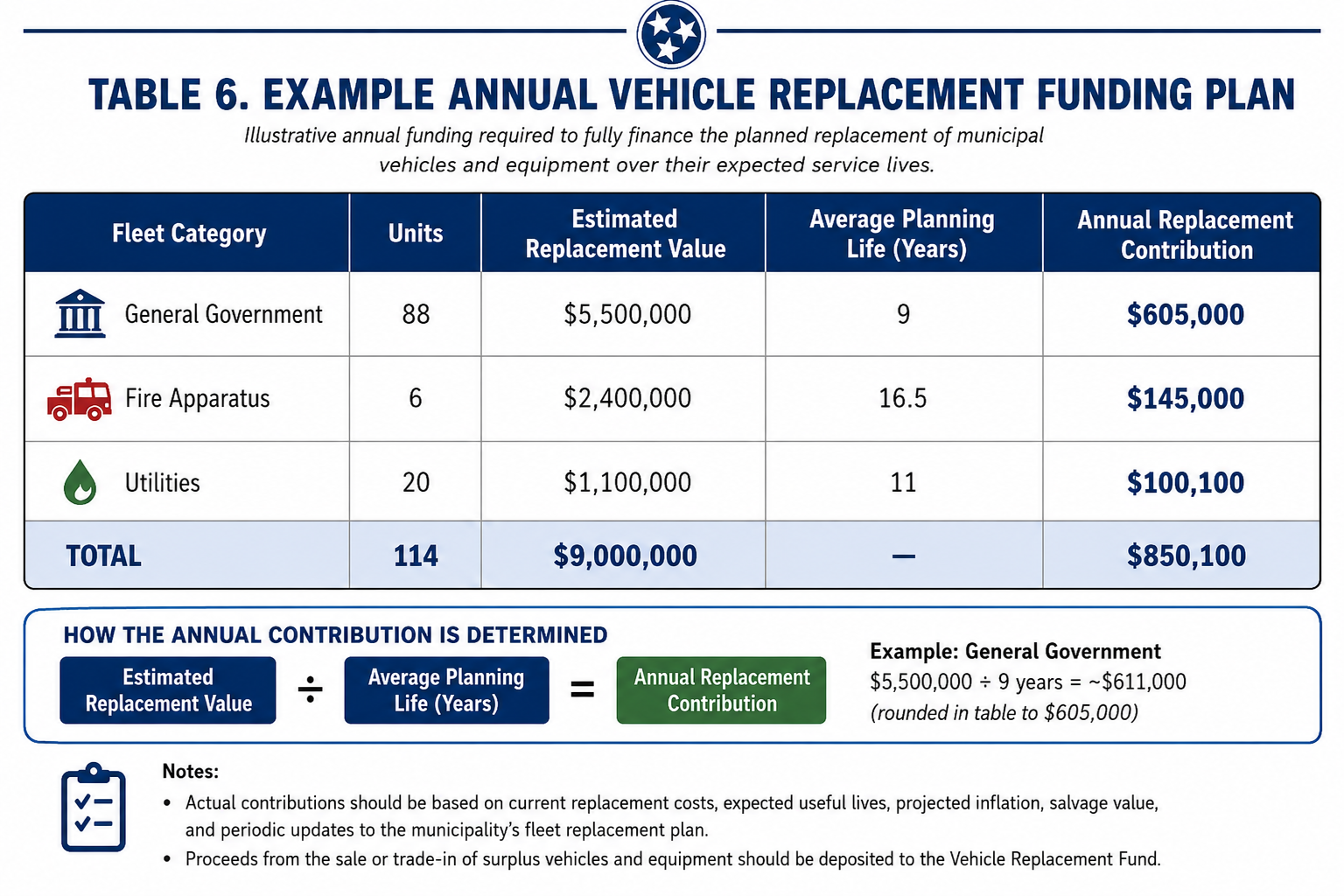

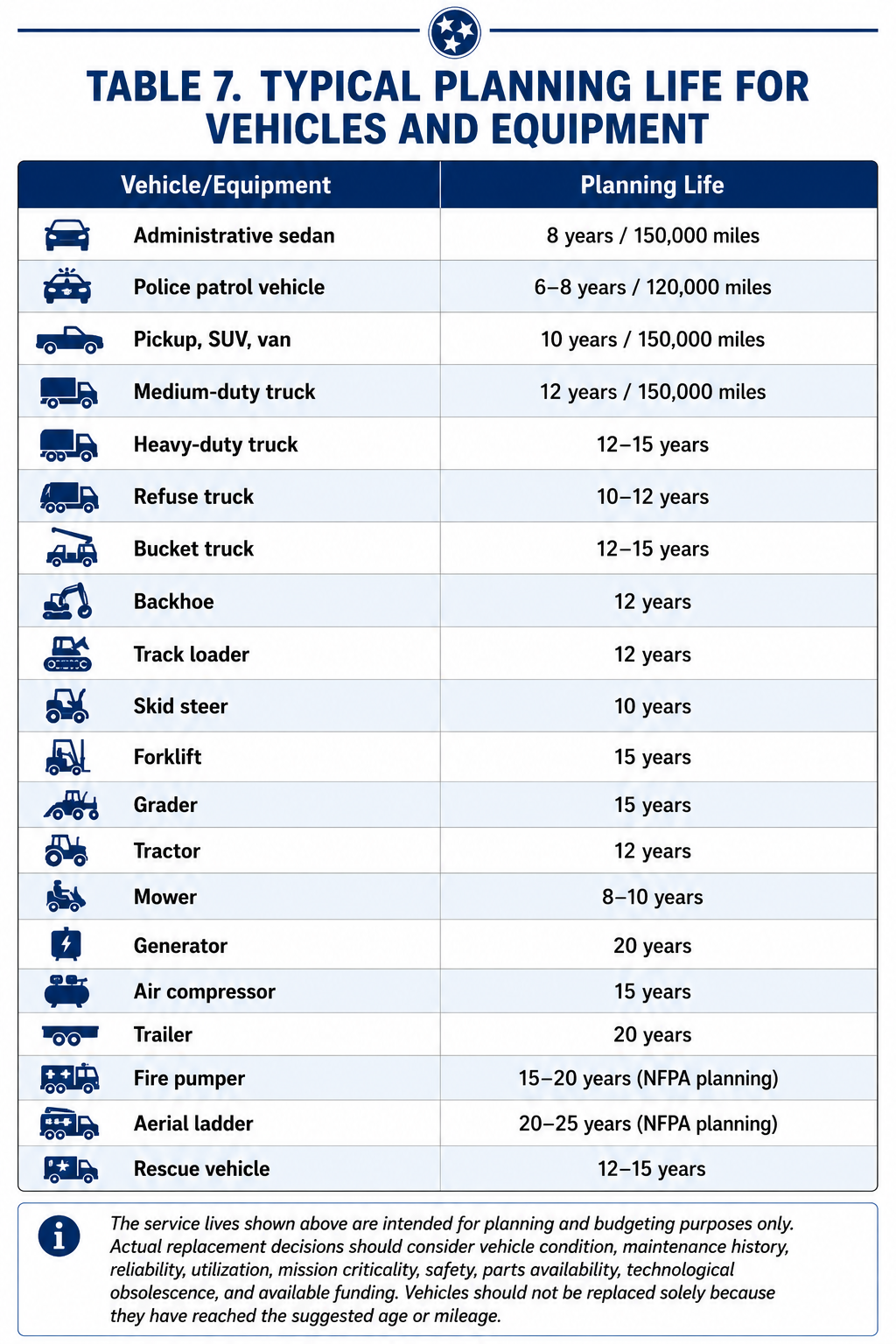

- Tables 6 and 7 illustrate a sample replacement funding schedule and typical planning assumptions for vehicle and equipment service lives.