Budget Calendar

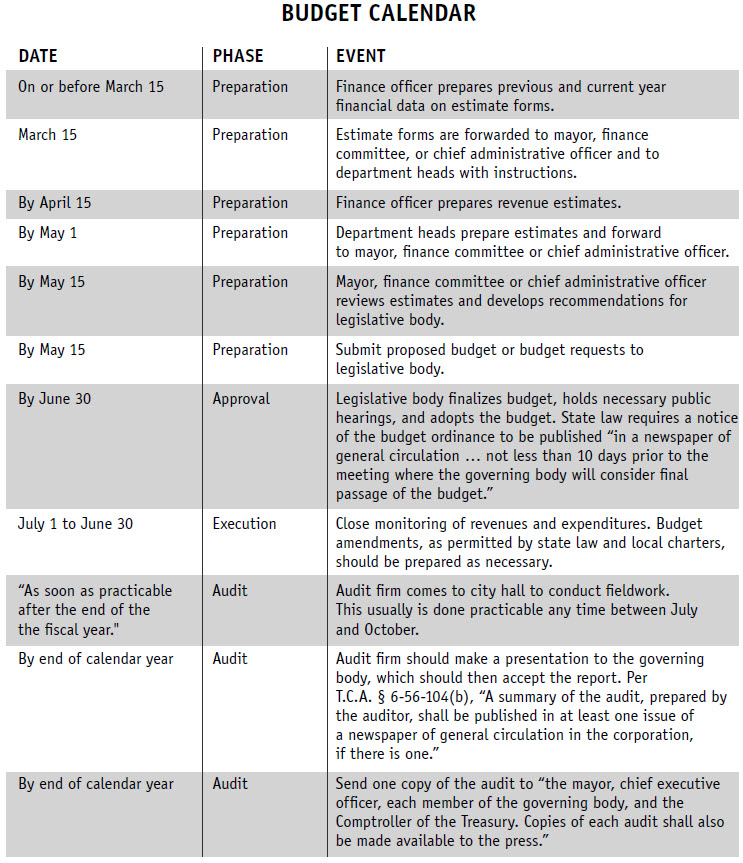

The budget cycle consists of four main steps or phases: preparation, approval, execution and audit. The audit, previously mentioned, is typically considered the last phase of the budget cycle; however, it is an integral tool in budget preparation. The following chapters describe in detail how to perform and prepare budget estimates.

The budget calendar is centered around budget adoption. Refer to the appendices for samples of required budget documents, including the public notice, the budget ordinance, and a few sample pages from a General Fund budget narrative (line item descriptions of the individual departments). Keep in mind that charters may vary as to publication and public hearing requirements so be sure to double check your charter before setting your budget calendar.

Below is a sample budget calendar for small- to medium-sized cities. The size, complexity, and any additional charter requirements of your municipality may change the preparation dates; however, the end of the fiscal year for Tennessee municipalities is June 30, and audits should follow closely thereafter.